Award-winning PDF software

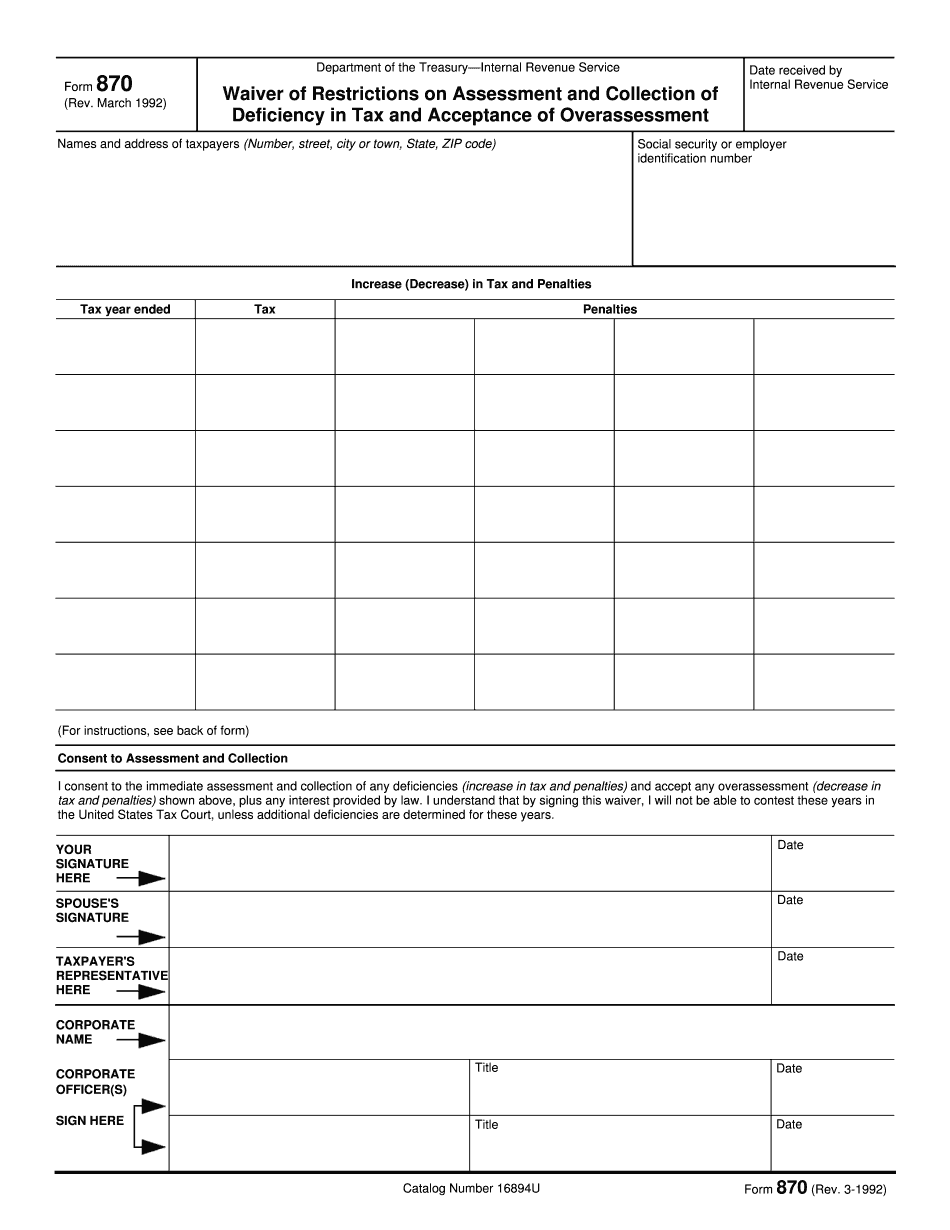

Seattle Washington online Form 870: What You Should Know

To the public” in the state of Tennessee: the business of supplying the public with goods or services at wholesale and retail. The Act also provided for a separate tax on the privilege of engaging in certain “special proprietaries” and exempted a substantial segment of the Tennessee population and commercial enterprises (those located within a defined geographical area) from this tax. A substantial segment of the population for this purpose is defined as not more than 25 percent of the population of the state as measured by the 2025 decennial census. The Act defined two types of tax exemption or relief from the tax, the most popular being the “exemptions for retail and wholesale” established in the 1976 Act. The Act then provided that a manufacturer, distributor, and dealer whose gross receipts do not exceed 30,000 annually in a tax year shall be liable for sales and use tax solely on the sales of taxable tangible personal property located, shipped, received, or consumed by such manufacturer, distributor, and dealer. In other words, manufacturers, distributors, and dealers that do not have any taxable sales can be exempt from the state sales tax and thus avoid the obligation to collect and remit the sales tax. The Act also provided for an exemption for manufacturers, wholesalers, and dealers by reference to the “suppliants for the exempt classes” established under the 1976 Act. In other words, if a dealer's gross receipts in any given tax year do not exceed 40,000, then that dealer is exempt from Tennessee sales or use tax and will not be subjected to filing any quarterly state income tax return. The Act also established a second class of exemptions, known as the retail sales tax exemption groups (REG): retail establishments with gross receipts of less than 20,000; and, if any REG has gross receipts of 35,000 or more in anyone tax year and is located in a county in which the sales tax is already paid by the manufacturer, distributor, or dealer, then the dealer's gross receipts do not have to be declared. If a dealer has receipts of up to 50,000 and is located in an area in which the sales or use tax is zero, then the dealer is exempt from sales or use tax but will be subject to any remaining obligation.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Seattle Washington online Form 870, keep away from glitches and furnish it inside a timely method:

How to complete a Seattle Washington online Form 870?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Seattle Washington online Form 870 aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Seattle Washington online Form 870 from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.